How To Fundraise in The Toughest Market in Two Decades (i.e., Relationship Selling 101)

Scott Barker breaks down how GTMfund raised a $54M Fund II

Hello and welcome to The GTM Newsletter by GTMnow - read by 50,000+ to scale their companies and careers. GTMnow shares insight around the go-to-market strategies responsible for explosive company growth. GTMnow highlights the strategies, along with the stories from the top 1% of GTM executives, VCs, and founders behind these strategies and companies.

How To Fundraise in The Toughest Market in Two Decades (i.e., Relationship Selling 101)

Last week, we could finally announce our second venture fund: GTMfund II. The news was picked up by TechCrunch, BetaKit, and many others.

Our initial target fund size was $50 million, and despite one of the most challenging fundraising environments for both funds and startups in recent history, we surpassed that goal, closing at $54 million.

Raising a fund, securing capital for a startup, or even selling into the enterprise all share a common foundation: relationship-driven sales.

Given how tough this market is, I figured it would be valuable to break down exactly how we did it.

At its core fundraising or selling comes down to three key priorities:

Building your network

Providing value to that network

Turning that value into pipeline

Anyway, let’s get into it.

The context

The background of Fund I

GTMfund’s first fund was a $22 million fund primarily backed by Operator Limited Partners (LPs).

Limited Partners: A partner in a company or venture who receives limited profits from the business and whose liability toward its debts is legally limited to the extent of his or her investment. For the purpose of this breakdown, I’ll use “Operator investor” synonymously.

Most of these LPs were C-Suite revenue leaders that Max Altschuler (GTMfund GP) and I had known for years so there was already a foundation of trust. You could think of this similar to a “friends and family round” or "founder-led selling” because these people already knew, respected and trusted us. While it wasn’t easy, many conversations moved quickly because tthey were primarily evaluating us based on: Our past accomplishments, Max’s angel investing track record, and their personal experiences with us.

These 300+ Operator investors became the core of our fund – our “product”. Calling close friends a “product” feels strange, but it’s true. What we had built was an ecosystem where knowledge and access flow from our Operator investors to our founders and their respective executive teams. And with all humility, it’s a damn good product.

Without their early support, we would not have had the same access to top tier software deals, the right to win competitive investments, and the ability to positively affect the outcomes of our companies once we invested. We are forever indebted to our early Operator investors. No matter how big we get, they will always get first right of refusal for investing in future funds.

That said, taking GTMfund to the next level required more capital. In order to raise 50M+, we needed to attract “institutional investors.”

Institutional Investor: A large organization, such as a bank, venture FoF, a large family office, pension fund, labor union, or insurance company, that makes substantial investments on the public and private markets. For the purpose of this breakdown, I’ll use “Institutional investor” synonymously.

Another way to think of this is that we were moving from selling to SMBs to selling into the Enterprise.

The challenge for raising Fund II

The problem? We spent our careers as operators, so our network naturally consisted of other operators and some venture capital connections from the companies we had previously been involved with. When it came to raising from larger institutional investors, we were navigating unfamiliar territory. This world can feel like a black box, where people keep their cards and connections very close to their chest.

The other major hurdle? You cannot openly market or solicit the fact that you are raising a fund.

Huh? So you’re telling me that I have to sell something that I’m not allowed to tell anybody about unless they specifically show interest first?

Max and I have always leaned heavily on marketing and media to drive outsized results. But this time, that tool was off the table.

The 7 steps we took to fundraise $50M+

Step 1: Clearly identify your strategy and unique differentiator

In the early days between Fund I and Fund II, we explored several different investing strategies. Thanks to our early success, we were fortunate to have access to many different opportunities. But looking back, this actually hurt us.

Just like in Enterprise Sales, you often get one shot with your prospect (or in this case, an investor). If you do not have your story or strategy completely buttoned-up,you're dead in the water.

Early on in a startup, it’s okay if the vision isn’t fully fleshed out before bringing on design partners or early customers. But if you’re selling a fund (or an enterprise deal), you’re selling a strategy and a solution that (ideally) the market does not yet have. You need to be crystal clear on what what you are, what you aren’t, and why you need to exist.

The big learning:

It’s one thing to talk about your “differentiator,” it’s another to show it.

One of our differentiators is go-to-market (GTM) support, so we offered that edge to investors in our pipeline. Did they have their own portfolio companies struggling with GTM? Well, let’s go and help them. This was common, and is now supported by data that shows that GTM is the number one worry and priority for founders.

Another major differentiator?

Our built-in distribution through our media company, GTMnow (shoutout to our VP of Marketing, Sophie Buonassisi!). Do they want to get their firm more exposure in the startup ecosystem? Awesome, let’s plug them into our media channels.

Step 2: Build a hyper-targeted list of potential investors

In other words, you need to define your ICP. Trying to broadly go after "institutional investors” is like saying we’re targeting the "enterprise market”.

If you're everything to everyone, you’re nothing to nobody.

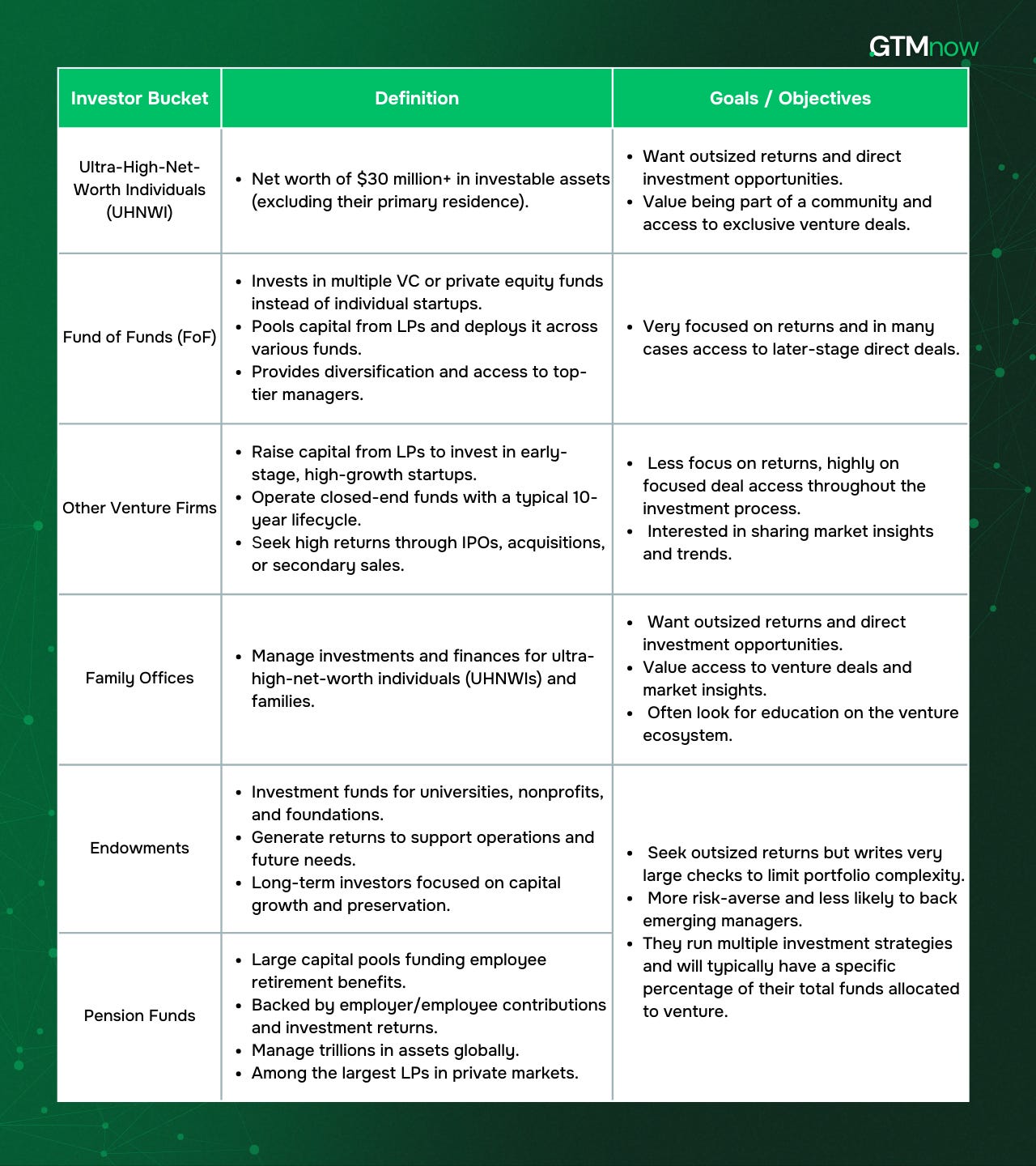

Institutional investors broadly fall into six buckets, which have slightly different objectives from their investment strategy.

Knowing what they want, you then need to have some really honest conversations with your team to understand who you serve best at this point in time.

For us, it was UWHNI, Funds of Funds, Venture Firms and Family Offices so that’s where we focused our efforts.

The actual list building process was difficult. It’s not as simple as buying a data provider license as many of these investors have a purposely low profile online and, quite frankly, don’t want to be found.

Our efforts required good old fashioned: Digging through Google, hounding our network, leveraging ChatGPT, monitoring X (Twitter), setting up Google alerts, and lots of LinkedIn sleuthing.

The big learning:

The best way to identify which investors are actually serious about deploying capital into “funds like you” is to talk to a lot of other “funds like you.” Some of the most valuable time I spent was with other Partners at similarly sized VC firms, swapping notes on different LPs. If a LP sounded promising, we would add them to the list or ask for an introduction.

I compare this to a Strategic Account Executive at a tech company: They will often connect with other Strategic AEs at non-competing companies with an overlapping ICP. Together, they can trade insights on their target accounts, priorities, and uncover net new opportunities.

Step 3: Warm introduction mapping

Ok, so the story and strategy are nailed and a list of high-potential investors is built. Now comes the hard part – getting in front of them.

We tried it all:

Buying a sales engagement platform and testing different messaging to book meetings. Since, we couldn’t openly say we were fundraising, the CTA had to be vague, which led to very low conversion rates.

Hiring an outsourced business development agency because we thought maybe our volume was just too low. Again, conversion was dismal.

Sending hundreds of connection requests on LinkedIn and X and trying to build relationships there. It worked to some extent, but clearly wasn’t going to get us to our target number.

Attending GP/LP introduction events – the high-ticket conferences designed to match investors and fund managers. I’m sure these work for some people, but for us, the power dynamics felt off from the start, and it often felt like we were starting these relationships on the back foot (Paul Irving and I even flew all the way to Hong Kong for a trade mission…).

For a few months, it felt like we were trying to scale an impenetrable wall.

The breakthrough

One thing became clear: Whenever we received a warm introduction from an existing LP, one of our founders or a friend of the fund, the meeting went extremely well and our conversion rate would be 10x.

We needed to find a way to scale our warm introductions.

Assisted by tools like Cabal, Sales Navigator, and way too many Google Sheets, we started to map out the different connection points we had with investors that were on that list.

We then prioritized those connection points based on the strength of relationship we had with that connection and the strength of the connection we believed they might have with that investor. Then we re-prioritized the list based on where we had the strongest in-roads into.

Then, I focused all of my fundraising time on three pillars:

1. Building up our network

This could mean hosting dinners and events, inviting guests onto The GTM Podcast, asking someone to contribute to this newsletter, interacting with others on social media, or showing up thoughtfully in other communities. The goal was to increase the surface area for warm introductions.

2. Providing value to that network

Everyone defines value differently, and the key was figuring out what mattered to each person. For some, it was introductions to peers. For others, it was connections to target accounts, sharing deal flow, or helping them fundraise. The rule of thumb was simple: five “gives” before ever making an “ask.”

3. Turning that value into pipeline

If you’ve genuinely provided value, people will usually become curious about your world. They’ll start asking questions that naturally lead to a commercial discussion. If not, by this point, you’ve earned the right to make the ask. So just ask.

When I was in fundraising mode, if an activity didn’t fit into one of these three pillars, I was likely just spinning my wheels.

The big learning:

Whether selling a fund, a service, or a product, we tend to over-index on the first and last pillar – building a network and then trying to turn that network into pipeline – while spending the least amount of time on the second, which is actually the most important.

Too often, we try to convert before we’ve earned the right to do so. The trust hasn’t been built yet. I’ve come to believe that the majority of time should be spent on pillar two: providing value.

It’s easier said than done because this part of the process doesn’t always feel like selling or fundraising. And when pressure is high, whether it’s a final close deadline or EOQ approaching, it’s the first thing to go. But ignoring it is a mistake. You have to learn to shut out the noise.

Maybe the value add doesn’t immediately move someone to the next step in your sales cycle, but it builds trust. And I agree with Benioff here:

Trust is the currency of business. No money changes hands without it.

At the end of the day, we’re all in the trust-building game.

Step 4: Nail the first meeting and follow up

Nail the first meeting

Skip the deck. Be curious. Have a real conversation.

This applies to Partners raising a fund, Founders raising capital (asterisk on this one as running through a few slides can be helpful when demonstrating a complex concept), and Enterprise sellers alike – nobody wants to sit through a slide-by-slide, canned pitch.

Send the deck ahead of time. It should tell the story on its own. Your job in the meeting is to tailor the conversation to the specific person you’re speaking with.

Like any good first meeting, the first half should be spent understanding their goals (both personal and firm-wide) and why they took the meeting in the first place.

For us, this meant digging into the history of the firm, their investment strategies, what’s been working for them, what they’re seeing in the market, whether they’ve invested in funds like ours before and where they see future opportunities.

Based on that, we would tell our story, spending more time on what they actually care about and cutting out the rest. Of course, leaving plenty of time for questions and next steps.

The data room and follow up

If the call goes well, typically they will ask for access to your data room.

For any first time managers out there, here is what we included in our initial data room:

A welcome video from our General Partner, Max

Our GTMfund II deck

Our fund model

Fund II deal breakdown - portfolio analysis

GTMfund Fund I metrics

Fund I portfolio companies

Fund II portfolio companies

Our GTMfund network

Everything should be up to date with the latest metrics so that you can follow up within 24 hours and ideally within the same business day. If they have bespoke requests, highlight those front and center in your follow-up email for easy access.

We used DocSend to track engagement because you can see who interacted with what, and for how long. This was a really helpful signal for identifying who was actually leaning in.

Finally, you’re going to have multiple versions of your data room.

The list above was our starting point, but we created custom data rooms for each institutional investor, adding new documents, analysis, and updates as we built them.

These custom data rooms took time and effort, so we never let that work go to waste. If one institutional investor had a question that led to a thoughtful multi-page response or analysis, we’d repackage and proactively send it to others in our pipeline.

It became a great excuse to re-engage with LPs.

For example:

"Jesse – we put together this exit scenario analysis for the fund and thought you might find it interesting. Just added it to your data room and included it here. Let’s catch up soon."

You’re constantly creating new proof points, new ammo for your data room. Make sure you’re leveraging all of it.

The big learning:

Many of these are all basic ‘sales best practices.’ Never cut corners on the basics, they are timeless fundamentals for a reason. Your process is a reflection of your product (fund). Every touch point is an opportunity to see how you and your team operate.

Step 5: The Diligence Process

Once a firm is seriously leaning in, they will put you through their “diligence process,” which can vary widely. Some can take 5 days, some can take 12 months.

Inevitably, there will be documents, reports, and analyses that, as an emerging fund, you won’t have on hand. But speed matters in this game. That often means late nights and weekend work to get them what they need as quickly as possible. (Shoutout to my Partner and Platform Director, Paul Irving, who carried the brunt of this).

I can tell you firsthand that hundreds and hundreds of hours went into a single diligence process to close one of our largest LPs.

Venture is a 10+ year partnership, so beyond the actual documents, investors are assessing your commitment, attention to detail, and ability to execute under pressure. That level of rigor and responsiveness de-risks you as a long-term partner.

How you do anything, is how you do everything.

Oh, and if you’re not ready to jump on a plane within 24 hours to meet them in person, you’re going to struggle. Shoutout to Max Altschuler for dropping everything and flying across the country multiple times to seal the deal.

The big learning:

Just like when we make an investment, we go through what’s called an Investment Committee (IC).

Investment Committee (IC): The governing body within a VC firm that evaluates and approves investment decisions before deploying capital into startups. The IC plays a critical role in portfolio construction, risk management, and capital allocation to ensure alignment with the fund’s strategy and LP expectations.

In other words, it’s a very important meeting (sometimes multiple meetings) where they decide whether or not to invest, based on everything they’ve learned through diligence.

Being on the other side of it, I now understand just how much work goes into putting together a deal memo, aggregating due diligence, and making the case for investment.

These investors are busy people, so you need to do as much of the work for them as possible.

We spent weeks creating a whitepaper that preemptively addressed every question we thought might come up in their IC meeting, so they walked in feeling fully prepared.

People have a lot going on, so reduce as much friction as you can.

One final note: Due diligence often means a lot of spreadsheets and numbers. Wherever possible, offer up founder and existing investor references. Those conversations bring the data to life.

At the end of the day, this is a relationship business.

Step 6: Staying top of mind and controlling the controllable

One of the most frustrating parts of raising capital was dealing with the uncontrollable – market conditions, deployment cycles, and timing misalignment.

There were plenty of times when we had multiple great conversations, everything looked promising, and then we’d hear that the timing wasn’t right.

Some common scenarios:

An institutional investor was also raising capital, and their first close wouldn’t happen before our final close.

They were already overweighted in their venture allocation for the year.

They were at the end of their deployment cycle, with the rest of their capital already committed elsewhere.

Whether it was the truth or just an objection, the "right place, wrong time" response is always tricky. It’s not a definite no, but it’s not moving forward either—so you’re forced into a balancing act of staying top of mind without coming across as overly needy.

I’m sure this sounds very familiar to sales reps and leaders reading this.

I tried to reframe these situations as simply buying more time to showcase who we are and why they should partner with us.

Never follow up just for the sake of following up.

This is when you go back to pillar two: providing value to your network.

If they’re looking for more direct access, send them a hot deal.

If they’re fundraising themselves, offer to make some introductions.

If they want market insights, share your latest thesis on a key vertical.

If they want to build their network in venture, invite them to a founder dinner you’re hosting.

Increase the value, increase the likelihood of conversion.

The big learning:

Treat people as if they are already a partner, and they’re much more likely to become one.

We send out detailed LP updates for our existing investors, so anytime we had someone in the pipeline, we made sure they were added to that distribution list.

This became a natural monthly touchpoint. It would spark curiosity, drive conversations, and keep us top of mind without forcing it.

Step 7: Building momentum and leveraging FOMO

Just like end-of-quarter in sales, when raising a fund, a large portion of capital typically comes in as you approach Final Close.

Final Close: The last fundraising milestone of a venture capital (VC) fund, after which no new Limited Partners (LPs) can commit capital to that specific fund. Once the final close occurs, the fund is officially closed to new investors, and the VC firm shifts focus entirely to deploying capital.

As you get closer, new conversations should slow down (for the most part), and your focus should shift entirely to converting the pipeline you’ve built. And you better have enough pipeline coverage to backfill anyone who won’t be ready in time.

A few months out, you should have a steady wave of positive data points to share with the investors in your pipeline. A new mark-up like Writer? New investors like HarbourVest?

The wave of momentum should be at its peak, and you want that to be felt across the board. This is the time to go all in.

At this stage, the mindset shifts from “providing value” to “driving towards a clear yes or no.”

This doesn’t mean burning bridges. Venture is a long-term game, and relationships matter. But at this point, both sides should be fully aware that the deadline is approaching.

You need to clarify where things stand. Is it a green light or a red light?

Time is not working in your favor, and prioritizing high-likelihood investors is critical when the shot clock is ticking. And even if it’s a red light, at least you understand why and can lay the foundation for future partnership opportunities.

One tactic that worked well when an investor went dark on us was backchanneling. Getting someone in their network to check in on our behalf often reignited stalled conversations.

The big learning:

In any fundraising or sales process, FOMO is real—and for better or worse, you should lean into it.

We all like to believe decisions are made rationally, but in reality, we’re all influenced by the people around us and the people we aspire to be like.

But here’s the key: you can’t manufacture FOMO on your own.

That feeling needs to be created by the people already invested in you—your founders, existing investors, or customers.

In other words, social proof creates FOMO.

Those voices are your most powerful tools, and your job is simply to amplify them.

⸺

That’s more or less the story. I hope that was valuable, or at the very least, an interesting read.

Over the past 18 months, I’ve sat through 400+ meetings, taken 43 flights, and spent countless nights stressing over hitting our fundraising goal. If nothing else, writing this out was a cathartic way to get some of the journey and lessons out of my head and onto digital paper.

Fundraising is a team sport, and none of this would have come together without the support of an incredible team, our operators/community, our founders, and hundreds of individuals who went out of their way to support us. Special shoutout to my friend Jason Demant at Foundation Capital for being an incredible partner who went above and beyond countless times.

Fundraising is hard.

Building a company is hard.

Selling is hard.

Hitting your number is hard.

And if you’re feeling stuck reading this, I see you.

During the tough moments, I often came back to this Charlie Munger quote:

“To get what you want, you have to deserve what you want.”

Put yourself in a position to deserve it. If you focus on the right actions every day, control the inputs, and manage the controllable, the universe will start to conspire in your favor.

Sometimes, it just needs a little time to catch up.

—Scott Barker

P.S. If you’re an operator looking for more investment-related material, check out our upcoming digital live event on angel investing.

Tag GTMnow so we can see your takeaways and help amplify them.

💡 GTMfund Toolkit

We’ve got the GTMfund team on Superhuman, which has been a game-changer for email efficiency.

Superhuman is generously offering the GTMnow community exclusive access to 1 month free on the platform. To claim this offer, go to www.superhuman.com/gtmnow

👂 More for your eardrums

Jordan Crawford is an AI innovator, the Founder of Blueprint, and one of the top go-to-market engineers working today.

This was a unique episode! It was super tactical and took a “show don’t tell” approach, with Jordan sharing his screen going through step-by-step how to prompt ChatGPT. Highly recommend watching on YouTube for this reason.

Jordan explains how to use AI tools like ChatGPT, Deep Research, and Claude to create your own AI workflow for prospecting accounts and creating highly targeted and extremely valuable messages for target decision-makers. Jordan also shares the prompts and processes he uses when researching target accounts, messaging buyers, and driving revenue.

Listen on Apple, Spotify, YouTube, or wherever you get your podcasts by searching “The GTM Podcast.”

🚀 Startup to watch

Houseware - just got acquired by LaunchDarkly. By joining forces, Houseware is bringing warehouse-native product analytics to a world-class platform used by over 5,500 enterprises including a quarter of the Fortune 500.

Tofu - announced a $12M Series A round. Tofu is working on cutting martech bloat, and this new capital will further these efforts and overall mission to build a unified AI platform for GTM teams.

Create - launched newly built in Postgres databases (powered by Neon) to make it even easier to go from “Text to App.” This enables impact to scale to millions of users. It might just be the fastest way to go from idea to full stack app on the planet.

👀 More for your eyeballs

Zero to $500M with Meka Asonye. This is the first part of a monthly series on the First Round Capital Review, called 0-$5M. Think of it as the early GTM brain trust you wish you had on speed dial.

Peter Walker of Carta’s playbook on how to create viral data storytelling. His posts on LinkedIn get thousands of likes and hundreds of comments and reposts. He pulls back the curtain on his playbook and how to run a successful data-driven content strategy.

Being CMO Under Marc Benioff of Salesforce. Plus, the “Innovator's Dilemma,” how pricing strategies are changing for AI products, and the impact of AI SDRs on pipeline.

🔥 Hottest GTM jobs of the week

Founding Account Exective - New Product at Gorgias (Toronto)

GTM Enablement Manager, Sales Development at Vanta (Hybrid - SF)

Growth Marketer at Tavus (Hybrid - SF)

Senior Manager, Demand Generation at Hone (Remote)

VP, Brand at Writer (Hybrid - SF)

See more top GTM jobs on the GTMfund Job Board.

If you’re looking to scale your sales and marketing teams with top talent, we couldn’t recommend our partner Pursuit more. We work closely together to be able to provide the top go-to-market talent for companies on a non-retainer basis.

📹 Upcoming digital live event

Angel Investing: On February 26th (and available on-demand exclusively for registrants), seasoned operator-investors will share how they got started, how they source and evaluate opportunities, what they’ve learned from their best (and toughest) investments, and more.

🗓️ GTM industry events

Upcoming go-to-market events you won’t want to miss:

The GTM Workshop for AI Founders (GTMfund event): March 25, 2025 (San Francisco, CA) - private registration

GTMfund Dinner: March 25, 2025 (San Francisco, CA) - private registration

More GTMfund events TBA

Spryng by Wynter: March 24-26, 2025 (Austin, TX)

Pavilion CMO Summit: April 17, 2025 (Atlanta, GA)

SaaStr Annual: May 13-15 (San Francisco, CA)

Web Summit: May 27-30, 2025 (Vancouver, CAN)

Pavilion CRO Summit: June 3, 2025 (Denver, CO)

Pavilion GTM Summit: September 23-25, 2025 (Dallas, TX)